- The share of new car buyers with a monthly payment of more than $1,000 jumped to a record high, according to Edmunds.

- With elevated prices and limited inventory due to supply chain challenges, the car market isn’t expected to improve anytime soon.

If you can even find a new car to buy, actually purchasing it is going to cost you.

"It's a really difficult time to buy a car," said Jessica Caldwell, executive director of insights at Edmunds.

Get Connecticut local news, weather forecasts and entertainment stories to your inbox. Sign up for NBC Connecticut newsletters.

Limited inventory due to a persistent shortage of computer chips, along with other supply-chain challenges, helped propel new car prices up 12.6% from a year ago and used car prices 16.1% higher, according to the latest data from the U.S. Bureau of Labor Statistics.

For new cars, the average transaction price is expected to reach an all-time high of $45,844 in June, according to a separate J.D. Power/LMC Automotive forecast.

Rising interest rates mean higher loan costs

Money Report

At the same time, financing any type of vehicle is also getting more expensive, as the Federal Reserve's latest interest rate hike of 0.75 percentage point pushes up the cost of auto loans.

"Low-interest rates used to be one of few reprieves for car shoppers amid elevated prices and supply shortages," Caldwell said. "But the Fed rate hikes this year are making finance incentives far costlier for automakers, and consumers are starting to feel the pinch."

More from Personal Finance:

Some experts see a recession coming

What people expect to spend more on as inflation surges

58% of Americans are living paycheck to paycheck

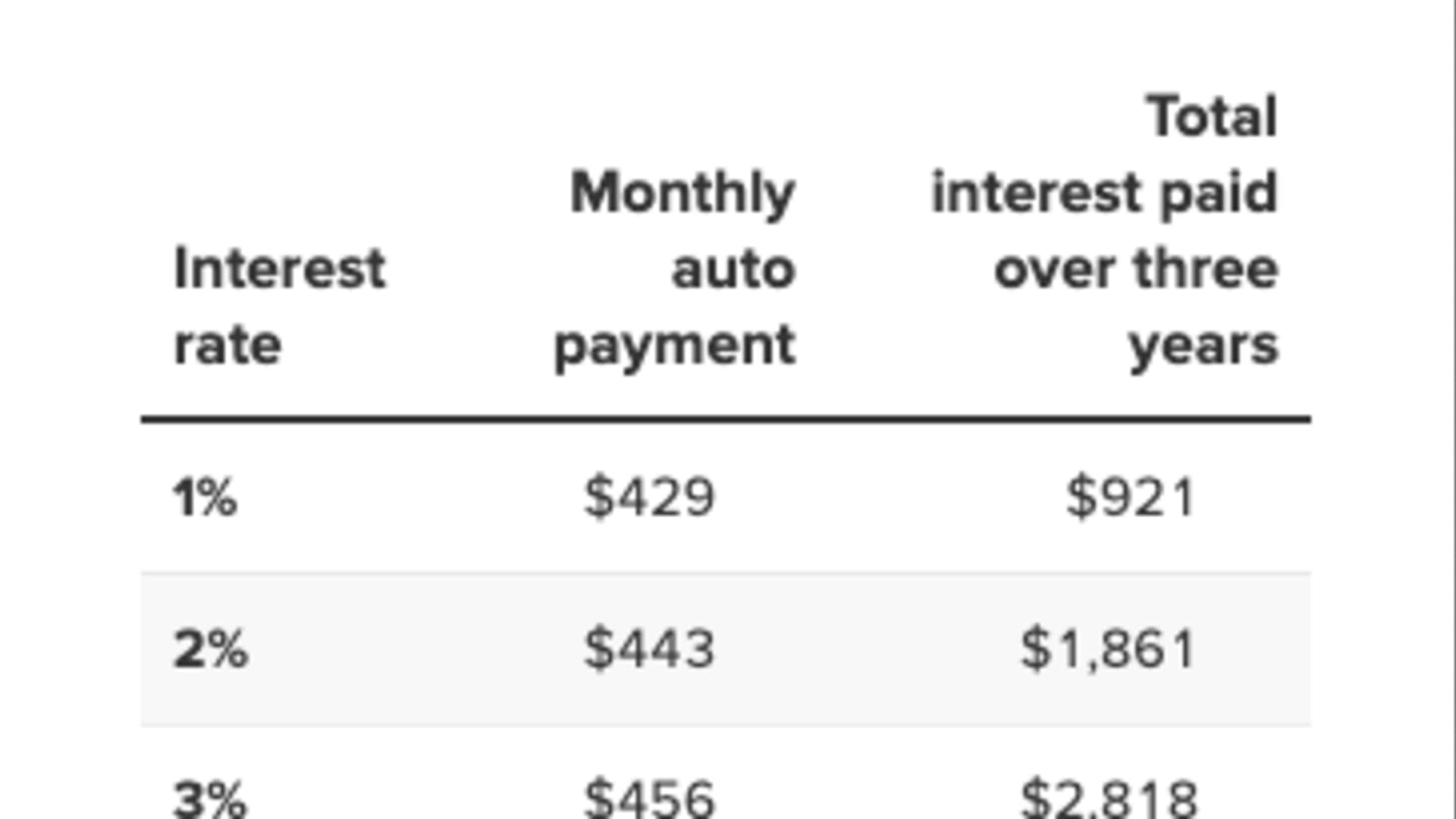

The average annual percentage rate on a new car hit 5% for the first time since the beginning of 2020, according to June data from Edmunds.

While an increase of about 1 percentage point may not seem like much, jumping to an APR of 5% from 4% could cost consumers $1,324 more in interest over the course of a $40,000, 72-month car loan, Edmunds experts said.

And still, luxury shoppers are flocking to dealerships, willing to spend more on high-end cars and the financing to go along with them.

For the first time, just over 12% of consumers who financed a new car in June committed to a monthly payment of $1,000 or more — the highest level on record — compared with 7.3% one year ago, Edmunds found.

"Although there appears to be a steady stream of affluent consumers willing to commit to car payments that look more like mortgage payments, for most consumers the new car market is growing increasingly out of reach," Caldwell said.

With the lucrative luxury SUV segment in high demand, more carmakers are upgrading their lineups and scaling back on smaller cars, Caldwell noted.

"There aren't a lot of options on the lower end."

Factoring in near record-high gas prices, the problem of affordability isn't expected to improve anytime soon, she added.

Typically, dealers offer some incentives to unload excess inventory before new models hit the lot, but not this year.

"Don't expect a lot of end-of summer sales; there's really no inventory to clear out at this point," Caldwell said. "If you want to wait for prices to get better, it will probably be a while."