What to Know

- The Federal Reserve left interest rates unchanged at the end of its two-day policy meeting.

- For consumers, it won't get any less expensive to carry credit card debt, buy a house, purchase a car or tap into home equity.

- Here's a breakdown of how the Fed's decision affects your money.

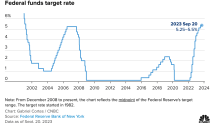

The Federal Reserve left its target federal funds rate unchanged for the second consecutive time Wednesday.

Even so, consumers likely will get no relief from current sky-high borrowing costs.

Get Connecticut local news, weather forecasts and entertainment stories to your inbox. Sign up for NBC Connecticut newsletters.

Altogether, Fed officials have raised rates 11 times in a year and a half, pushing the key interest rate to a target range of 5.25% to 5.5%, the highest level in more than 22 years.

"Relief for households isn't likely to come soon, at least not directly in the form of a cut in the fed funds rate," said Brett House, economics professor at Columbia Business School.

Money Report

The consensus among economists and central bankers is that interest rates will stay higher for longer, or until inflation moves closer to the central bank's 2% target rate.

What the federal funds rate means for you

The federal funds rate, which is set by the central bank, is the interest rate at which banks borrow and lend to one another overnight. Although that's not the rate consumers pay, the Fed's moves still affect the borrowing and savings rates they see every day.

To a certain extent, many households have been shielded from the brunt of the Fed's rate hikes so far, House said. "They locked in fixed-rate mortgages and auto financing before the hiking cycle began, in some cases at record-low rates during the pandemic."

However, higher rates have a significant impact on anyone tapping a new loan for big-ticket items such as a home or a car, he added, and especially for credit card holders who carry a balance.

Here's a breakdown of how it works.

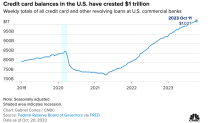

Credit card rates are at all-time highs

Since most credit cards have a variable rate, there's a direct connection to the Fed's benchmark. As the federal funds rate rose, the prime rate did as well, and credit card rates followed suit.

Credit card annual percentage rates are now more than 20%, on average — an all-time high. Further, with most people feeling strained by higher prices, more cardholders carry debt from month to month.

"Rising debt is a problem," said Sung Won Sohn, professor of finance and economics at Loyola Marymount University and chief economist at SS Economics.

"Consumers are using a lot of credit card debt and paying very high interest rates," Sohn added. "That doesn't bode well for the long-term economic outlook."

For those borrowers, "interest rates staying higher for a longer period underscores the urgency to pay down and pay off costly credit card debt," said Greg McBride, chief financial analyst at Bankrate.com.

Home loans: Deals slow to 'standstill'

Although 15-year and 30-year mortgage rates are fixed and tied to Treasury yields and the economy, anyone shopping for a new home has lost considerable purchasing power, partly because of inflation and the Fed's policy moves.

The average rate for a 30-year, fixed-rate mortgage is up to 8%, the highest in 23 years, according to Bankrate.

"Purchase activity has slowed to a virtual standstill, affordability remains a significant hurdle for many and the only way to address it is lower rates and greater inventory," said Sam Khater, Freddie Mac's chief economist.

Other home loans are more closely tied to the Fed's actions. Adjustable-rate mortgages and home equity lines of credit, or HELOCs, are pegged to the prime rate. Most ARMs adjust once a year after an initial fixed-rate period. But a HELOC rate adjusts right away. Now, the average rate for a HELOC is near 9%, the highest in over 20 years, according to Bankrate.

Still, Americans are sitting on more than $31.6 trillion worth of home equity, according to Jacob Channel, senior economist at LendingTree. "Owing to that, many homeowners could benefit from tapping into the equity they've built with a home equity loan or line of credit."

Auto loan payments get bigger

Even though auto loans are fixed, payments are getting bigger because prices are rising along with the interest rates on new loans, pushing up costs for car buyers.

The average rate on a five-year new car loan is currently 7.62%, the highest in 16 years, according to Bankrate.

More from Personal Finance:

62% of Americans live paycheck to paycheck

Why working longer is a bad retirement plan

Credit scores hit all-time high as households fall deeper in debt

Now, more consumers face monthly payments that they likely cannot afford. However, experts say consumers with higher credit scores may be able to secure better loan terms or shop around for better deals.

Car buyers could save an average of $5,198 by choosing the offer with the lowest APR over the one with the highest, according to a report from LendingTree.

Student loans: New borrowers take a hit

Federal student loan rates are also fixed, so most borrowers aren't immediately affected by the Fed's moves. But undergraduate students who take out new direct federal student loans are now paying 5.50% — up from 4.99% in the 2022-23 academic year and 3.73% in 2021-22.

The government sets the annual rates on those loans once a year, based on the 10-year Treasury.

If the 10-year yield stays near 5%, federal student loan interest rates could increase again when they reset in the spring, costing student borrowers even more in interest.

For those with existing debt, interest is accruing again, putting an end to the pandemic-era pause on the bills that had been in effect since March 2020.

So far, the transition back to payments is proving painful for many borrowers.

Savings account holders are earning more

"Borrowers are being squeezed, but the flipside is that savers are benefiting," McBride said.

While the Fed has no direct influence on deposit rates, the yields tend to be correlated to changes in the target federal funds rate. The savings account rates at some of the largest retail banks, which were near rock bottom during most of the Covid pandemic, are currently up to 0.46%, on average, according to the Federal Deposit Insurance Corp.

"Average rates have risen significantly in the last year, but they are still very low compared to online rates," added Ken Tumin, founder and editor of DepositAccounts.com.

Some top-yielding online savings account rates are now paying more than 5%, according to Bankrate, which is the most savers have been able to earn in nearly two decades.

"Savings are now earning more than inflation, and we haven't been able to say that in a long time," McBride said.

Don't miss these stories from CNBC PRO:

- Bank of America's investment strategist says the S&P 500 correction could last until it hits this level

- A 'panic spike' is possible late October into November, says Bank of America's chart analyst

- The S&P 500 has entered a correction. Here's why Warren Buffett likely thinks that's good news

- Morgan Stanley auto analyst Jonas says investors are 'waking up' to idea that Ford, GM are not a way to play EV boom