- Interest rates for credit cards are likely to continue at elevated levels for the rest of 2024, even if the Federal Reserve cuts rates.

- Rates for savings accounts continue to be high, but likely won't stay there for much longer.

- Rates for home mortgages could continue moderating as the year progresses.

Inflation in the U.S. has hit a speed bump.

While the rate of price increases has come down significantly from its peak in the summer of 2022, the most recent reading from the consumer price index showed overall inflation stuck at just above 3%.

Get Connecticut local news, weather forecasts and entertainment stories to your inbox. Sign up for NBC Connecticut newsletters.

Core inflation — which removes volatile food and energy prices from the index — was even higher, at 3.8%.

For perspective, the Fed's inflation target is 2%.

Those higher-than-expected readings dashed most hopes that the U.S. Federal Reserve would begin cutting interest rates this spring, as many central bank watchers hoped they might after nearly two years of steady rate increases.

Money Report

More from Personal Finance:

Here are 3 key things to know with one month until the tax deadline

The best time to sell your home. In 2023, listings in this period sold for more

What is shrinkflation? Why consumers may be getting less for their money

For everyday consumers, that means most interest rates will continue at their decadeslong high for a little bit longer. But while the Fed has now left rates untouched since July, consumers have still seen some movement in rates on common products like mortgages and credit cards due to other influences.

Here's what those high rates have looked like over the past 12 months in four major consumer categories: savings accounts, certificates of deposit, credit cards and mortgages.

Savings accounts

Higher rates mean that consumers have to pay more to service their debt, but it also means that banks pay higher rewards to savers. It's one of the silver linings to the current rate environment, said Ted Rossman, chief credit card analyst at Bankrate.

"There's also been remarkable stability at the top of this market," Rossman said. "The highest savings rate right now is 5.35%."

That top rate is considerably higher than the national average for savings rates overall, which has been just below 0.6% for the past two months. But even that overall average is more than double its level of 0.23% 12 months ago.

Rossman added that plenty of high-yield savings accounts, mostly available online, are still paying close to or even above 5%. These kinds of accounts keep money easily accessible while earning solid returns and are great options for emergency savings.

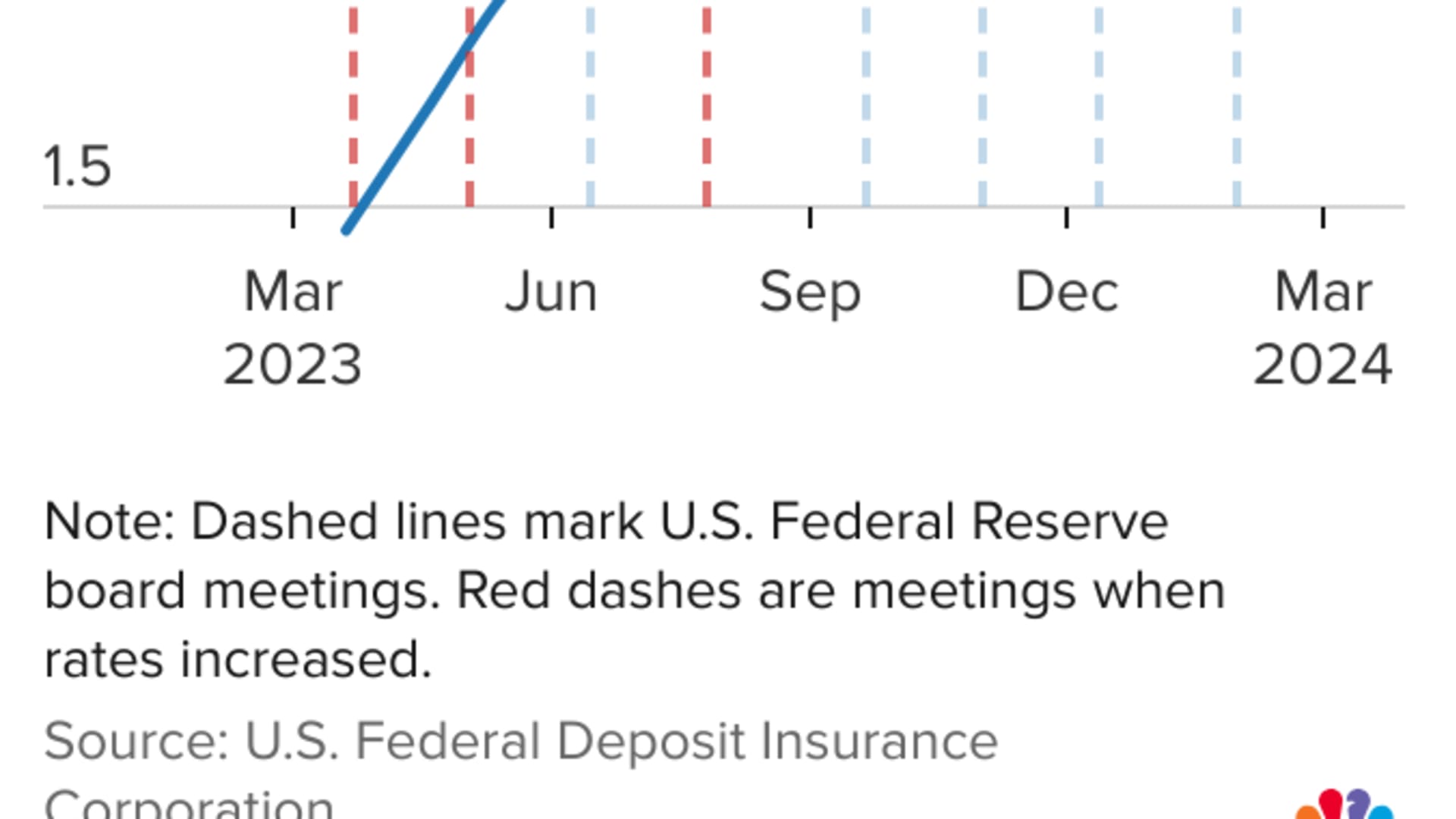

Certificates of deposit

Interest rates on savings accounts are higher than they've been in decades, but there has been recent softening in returns on certificates of deposit, data from the U.S. Federal Deposit Insurance Corp. shows.

The average yield on a 12-month certificate in March 2024 was 1.81%, down slightly from its high in December and January, according to the FDIC.

Despite the dip, CDs are good savings vehicles that avoid risk but still provide a return if you're willing to tie up your money for a set period of time, Rossman said. The current environment will likely remain good for savers until the Federal Reserve initiates its rate cuts.

"There's been remarkable stability at the top of this market, even though we expect cuts are coming," he said. "These shorter-term rates don't tend to move until the Fed moves."

Until then, savers should take full advantage.

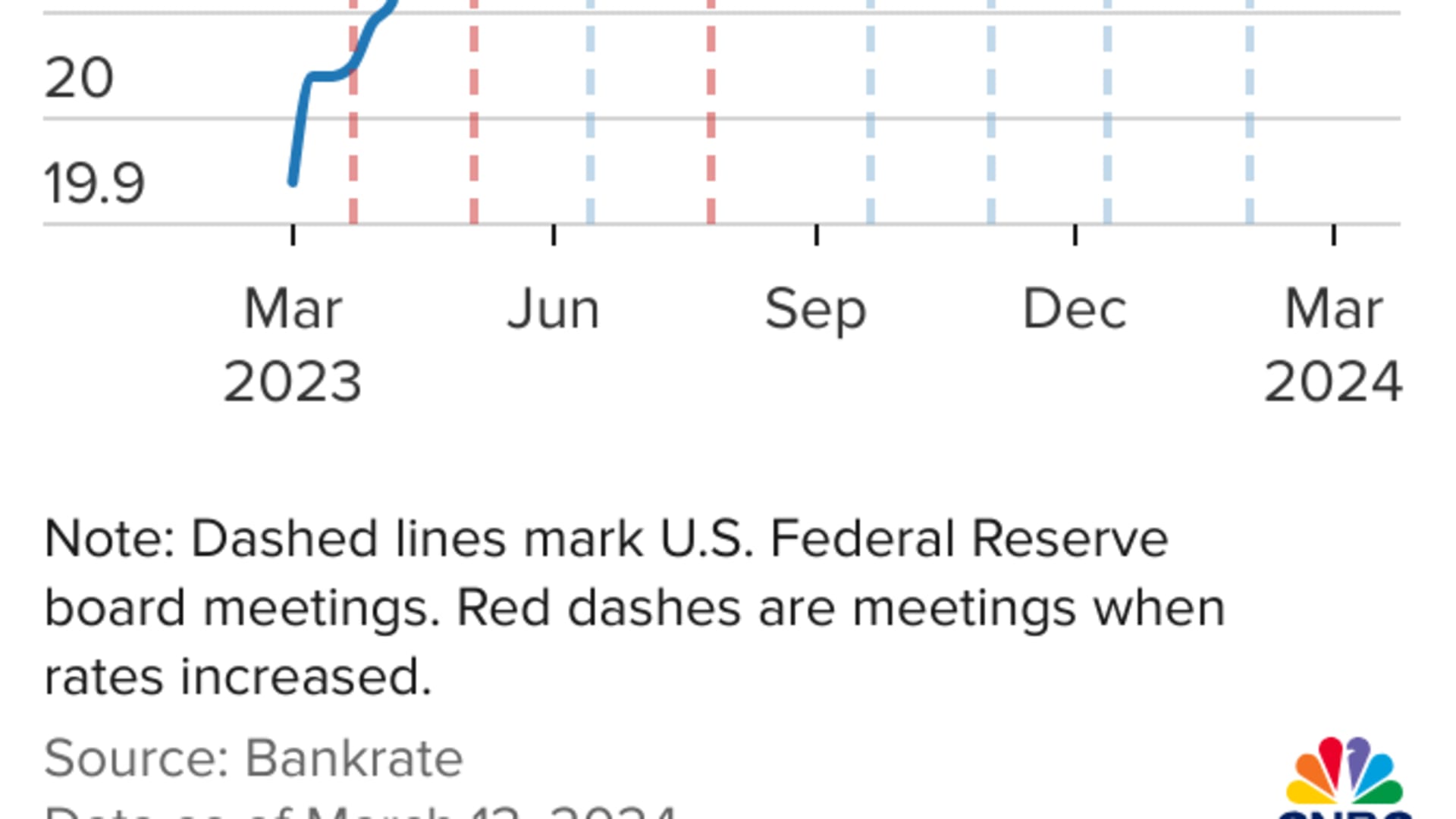

Credit cards

The flip side to the positive environment for savers is the expensive credit card market: Consumers carrying balances on their cards face historically high rates. The average credit card rate has been well above 20% for the past 12 months and will continue to stay there for some time, Rossman said.

"Sometimes rates bounce around a little bit if offers come on and off the market," Rossman said, but "we've plateaued since that last rate hike as of late July."

The key for consumers to remember is that credit card debt is expensive, and that will still be true even after the rate cutting starts, he said.

"The Fed is not going to come to your rescue on credit card rates," Rossman said. "Even if rates fell a couple of points in a couple of years, they'd still be high."

His best advice for consumers is to prioritize paying off credit card debt, if possible with the help of a balance transfer card, which lets consumers carry balances from one credit card to another for a low fee and an extended period of no or low interest.

Rossman added the offers from balance transfer cards continue to be very favorable with low fees and generous repayment windows.

"The balance transfer market has been remarkably stable and strong," he said. "It speaks to a strong job market and the strong economy. People are paying these bills back," despite the fact that more consumers, on average, are carrying more expensive debt.

Mortgage rates

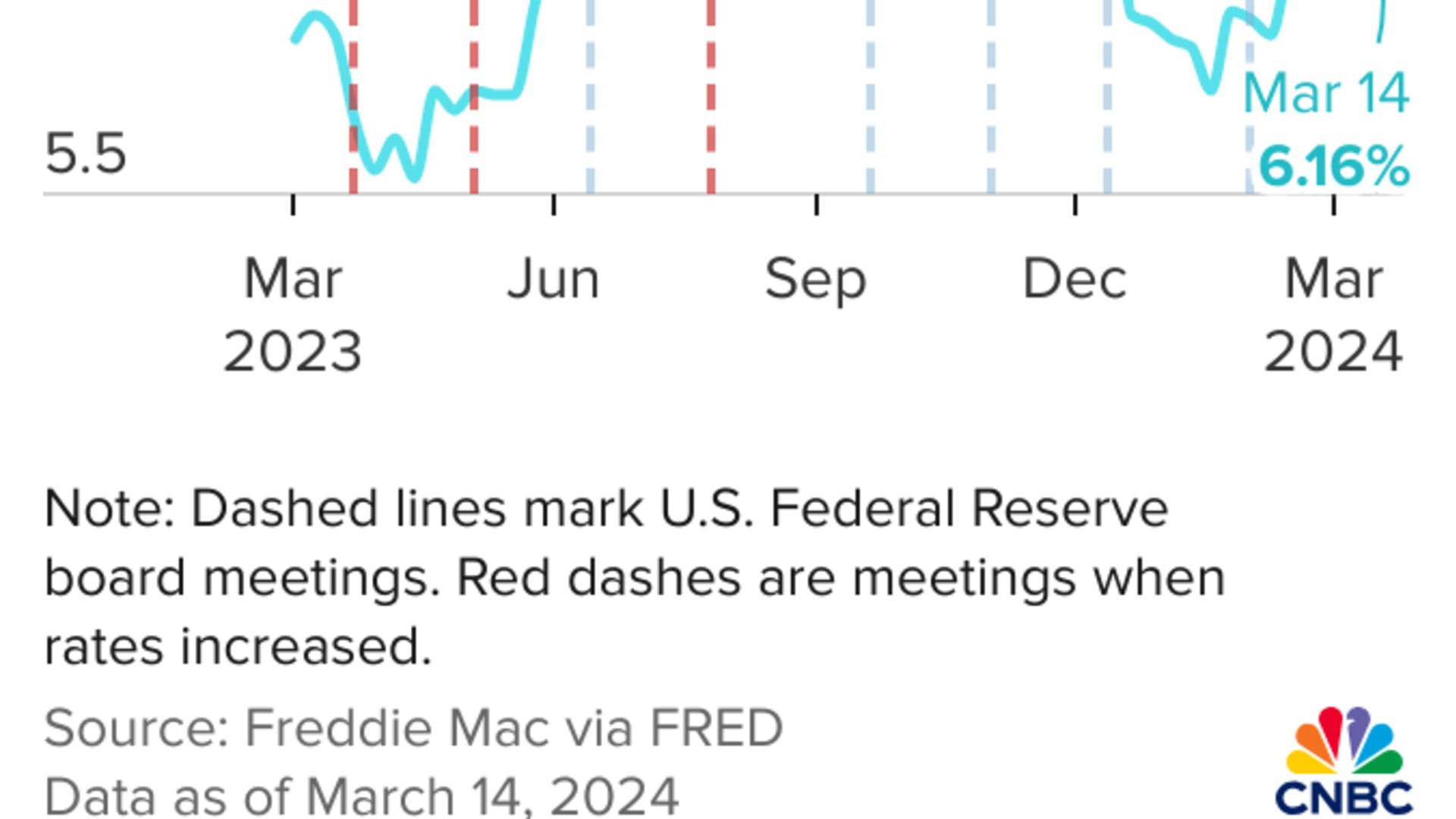

While savings and credit card rates are very sensitive to maneuvers from the Federal Reserve, the area that might see the most movement is housing.

"Unlike some of these other products, mortgage rates tend to move in advance of the Fed because they tend to track 10-year Treasurys," Rossman said. "It's more about investor expectations for the Fed and for economic growth."

That's reflected in the data. Mortgage rates peaked in October 2023 at about 8%, followed by a steady decline. And after a brief jump in February, they seem to be settling back to where they were at the beginning of 2024, when a 30-year fixed rate mortgage was about 6.6%.

"We think there's a good chance that the average 30-year fixed rate mortgage could be around 6% by the end of the year," Rossman said, which would be a much needed reprieve for a highly competitive housing market that is still undersupplied.

High mortgage rates have kept many sellers — who are locked into lower rates from years' past — from putting their homes on the market. Lower rates could get them to list, Rossman said.

"The closer we get to 6% and then eventually into 5% territory, that gets some people off the fence and they list their home and then inventory improves," he said. "Then that gives some some relief on the price side for would-be buyers."